GIA vs SIPP vs ISA: Tax Comparison

The right assets in the right accounts

The differential in the amounts of tax paid on income versus capital gains should be a key consideration when creating a portfolio across multiple accounts such as a Self investment Personal Pension (SIPP), General Investment Account (GIA) and Individual Savings Account (ISA) and deciding which investment assets should go in which accounts.

Example

According to FE Trustnet as of the 6th April 2021, the three-year return on the HSBC FTSE ALL World Index for a sterling investor was 44%, of which approximately 6% was earned as dividends and 38% came from capital gain.

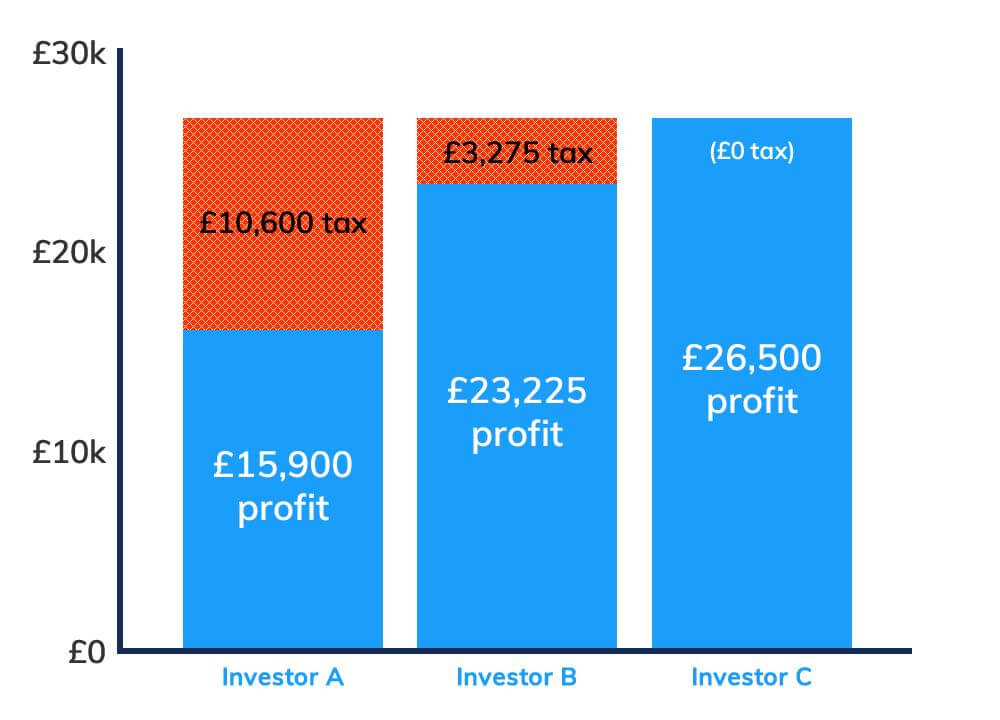

An investor who put £50,000 into the accumulation units of this on the 5th April 2018 would have £72,000 as of 6th April 2021, making a profit of £22,000.

The after tax profits of three types of investor

Investor A put the investment into her flexible drawdown SIPP, having already drawn the tax-free cash sum, and from where she regularly draws more than the higher rate tax band of £50,270 p.a. She wants to draw the profit out to spend it and would pay 40% income tax: £8,800 tax.

Investor B put the investment into his GIA. As a 32.5% income tax payer he would pay £975 in income tax on dividends earned. If he made no other capital gains that year he would pay £1,340 in capital gains: £2,315 tax in total.

Investor C put the investment in the GIA of his partner who earned no other dividends, and then split the holding with his partner before sale. Neither of them made any other capital gains in the year, and so would pay no capital gains and no tax on dividends: zero tax.

Paying less tax means higher after-tax spendable income or more retained capital.

Important Notes

Tax issues will depend on everyone’s individual circumstances. Future tax rates, allowances, tax types and the tax treatment of savings and pension accounts will be subject to change. Tax planning needs to be a regular ongoing process.

Non UK resident tax payers will need to get advice on the taxes payable in their country of residence.

Tideway are not tax advisers and if you have any doubt, you should seek specialist tax advice.