After a stellar year for investment markets in 2021, the past 20 months have certainly been a very challenging period for investors with the Russia-Ukraine war, sky high inflation and rapidly rising interest rates causing significant investment market volatility.

Global equity markets have barely produced a positive return and fixed income has suffered greatly, with UK Gilts down some 25% since January 2022.

Despite this poor period for the capital value of investments, the past 20 months has actually been a great period for those investors looking to generate an income in retirement and, for periods like this, having a wealth manager adds incredible value to enable you to achieve your financial goals.

With UK interest rates now at 5.25%, up from 0.25% in January 2022, investors can finally generate a meaningful income from their savings, albeit still below that of inflation – hopefully this will not be the case by the end of the year, as inflation continues to fall.

People can easily receive 5% on their cash savings and a little more if they are willing to tie their money up for a year or so. But crucially, for those who have money in pensions, ISAs or other accounts, the income that can be generated by investments is now higher than it has been since the financial crisis of 2008.

However, despite the much-improved environment for generating an income from investments, the past 20 months has generally seen a reduction in most tax allowances:

- Personal Allowance – a minuscule increase to £12,570 (up from £12,500 in January 2021)

- Dividend Allowance – this is currently £1,000 (down from £2,000 in January 2021) and will reduce to £500 in the 2024/25 tax year.

- Capital Gains Tax Allowance – this is currently £6,000 (down from £12,300 in January 2021) and will reduce to £3,000 in the 2024/25 tax year.

So, where does this leave investors today looking to generate a tax efficient income in retirement after this mixture of poor investment returns, lower tax allowances but higher interest rates?

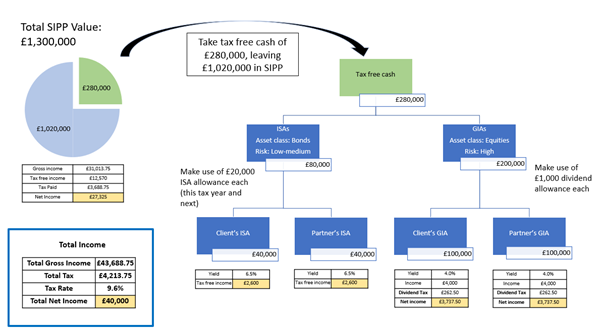

Let’s review an example: John is 56, married, has a SIPP worth £1.3m, has Individual Pension Protection that allows him to take a tax free lump sum of £280,000 and he would like to draw an income of £40,000 net p.a. How can this be generated from the different accounts – SIPP, ISAs and a General Investment Account (GIA)?

This can be the strategy:

John is in a better position in the following ways:

- The income from the ISAs is now £5,200 – up from £4,000 (yield was 5.0%, now 6.5%).

• The income from the GIA is now £8,000 – up from £4,000 (yield was 2.0%, now 4.0%). - Although John and his wife now have to pay dividend tax of £525 (assuming she is a basic rate taxpayer), the net income is still far higher at £7,475.

- By generating and drawing a much higher level of income from the ISAs and GIA, John now only has to draw an income of £31,013.75 gross from his SIPP, rather than £37,875 in January 2021.

- John therefore pays less tax on his pension income and he pays less tax overall, despite a higher tax environment; the overall tax rates drops from 11.3% to 9.6%.

- John does not need to touch the capital from his portfolio; the income generated from the investments is greater than his income needs – John should spend more money and enjoy his retirement!!

So, despite an unsettling period both in terms of investment markets and tax allowances, people now looking to draw an income in retirement are in a far better position than in January 2021 and even for the past 15 years.

At Tideway, we ensure that our clients have strategies like this to help them secure their retirement, not only for a couple of years but for the long term. If you know anyone who could benefit from having a conversation about how to generate income in retirement, please forward this email or share our details with them.