It would be a true statement to say we are happy to see the end of Q1 2022 with significant market volatility causing headaches for asset allocators. As has been consistent throughout the quarter, the main points of interest continue to be inflation, including central bank messages and policy responses and the Russo-Ukrainian war which has only served to exacerbate the former. China’s zero Covid policy and almost historic volatility in the tech sector (dot.com level moves) of their equity markets has also given pause for thought.

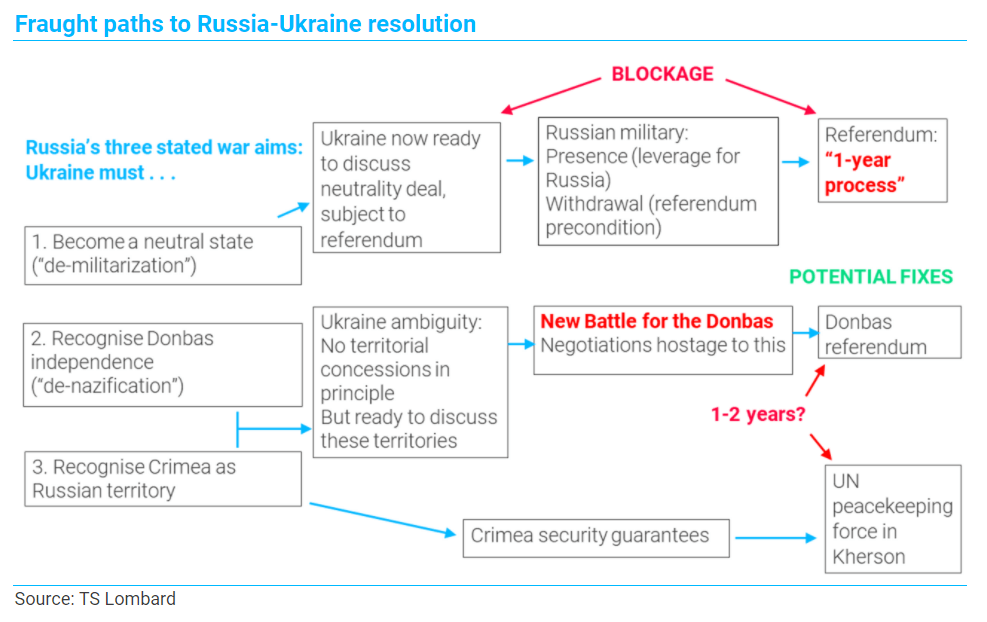

As per usual we will be producing your quarterly valuations over the coming weeks which will include a commentary analysing performance and will highlight any key winners or losers over period. With this in mind, we will try not to duplicate this work here, but instead to focus on the events in Russia and Ukraine (see TS Lombard flowchart). Being so intertwined with rising yields and policies of central banks, we will take this opportunity to provide an update on the fixed income portion of portfolios discussing positioning and highlighting some considerations. Valuations will be available in your portal in around ten days to two weeks’ time. The market commentary can be requested directly from your wealth manager from early next week should you wish to review in advance.

There has been some respite over the last few weeks with markets trending upwards. Equity markets in particular have recovered well off their lows with the US close to all-time highs due to relative lack of exposure to the fallout of the Russo-Ukrainian war. Despite prices appearing higher on our screens than a few weeks ago, we remain relatively sanguine. We are aware, that despite perceived improvement of underlying market conditions, things can change quickly. As TS Lombard explain in the section below, any resolution to war is not that simple.

We remain focused on aspects of the portfolio within our control by keeping up to date with our existing managers as well as meeting new managers for both comparison and competition as well as regularly discussing longer-term asset allocation decisions.

Russo-Ukrainian War:

In a major war, markets typically move prior to war breaking out and then find a bottom within the first ten days. Even though the second order effects of this war may prove more damaging, as with past wars this has proven relatively accurate thus far. This has been more acutely felt in Europe reflecting economic sanctions and potential shortages due to current reliance on Russian Oil & Gas. By contrast, US markets with their relative lack of exposure, are not far off their all-time highs.

This recent recovery in equity markets has coincided with some ‘positive’ noises from the Russian side. There has been an increased willingness to engage in more constructive peace talks with some of the initial demands delivered at the outset of Putin’s special military operation beginning to be dropped. Despite this seemingly positive news Christopher Glanville, Managing Director, EMEA and Global Political Research at TS Lombard, notes, ‘although both sides now appear to be serious about trying to find a negotiated settlement, there is still a ‘mountain to climb.’’

Further positive news out the Russian camp indicates that military operations around cities in North-East Ukraine will be wound down with focus on “protecting and liberating” the Donbas. Despite the market reacting positively we remain quite cautious with Putin having proven he is more than able to fool consensus. Christopher Glanville further notes that even if the ‘The key judgement rather is that even if today’s negotiating progress is built on, the necessary steps in the conflict resolution process that are now becoming clear will take a year or two to implement.’ The flowchart below, courtesy of TS Lombard, most succinctly summarises the situation and for us reiterates that we should not be getting ahead of ourselves.

Central Bank Policy and Rising Rates:

As expected, central bank policy responses to inflation, have had a negative effect on fixed income strategies with senior reporter, Abraham Darwyne of FE Trustnet, stating that over 95% of bond funds are in negative territory year to date. This should not come as a surprise with volatility increasing in the more duration sensitive areas of the asset class a result of US monetary policy looking to return to ‘neutral’ more quickly than the markets were anticipating. Courtesy of Juan Valenzuela, manager of the Artemis Target Return Fund noting latest Fed policy and its potential implications.

‘The probability of a recession over the coming 24-36months has unquestionably increased. Ultimately the Fed is telling us that they are looking to tighten policy beyond the neutral level (Fed sees neutral around 2.5%) – so they are taking policy to restrictive territory. By definition the risk of the Fed overcooking policy (therefore causing a recession) has to be higher all things equal. This in itself does not mean that the risk of recession is high.’

‘The Fed needs to control inflation, or they run the risk of inflation expectations getting un-anchored. They cannot risk their credibility. Currently, inflation goes beyond economics, it is a political issue.’

The fixed income managers Tideway have employed are in negative territory year to date, though we believe our positioning within the asset class has been broadly sound avoiding some of the hardest hit areas whilst being able to benefit from higher rates going forward.

Fixed Income Positioning:

We retain minimal exposure to government securities (Artemis Target Return can purchase if they believe there is relative value) believing them to be a source of return free risk especially as their correlation to Equities has turned positive in line with their longer-term historical relationship. This is significant, as holding government securities has been the primary way most asset allocators have been able to hedge their portfolios. Should investors have continued with this methodology in 2022 their results will have been poor returning -7.34% (IA Gilts), whilst still offering relatively (compared to Credit) low yields.

| Fund Name | YTD |

| Royal London Sterling Extra Yield Bond | -1.73% |

| Artemis Target Return Bond | -2.11% |

| Artemis (Lux) Short-Dated Global High Yield Bond | -2.13% |

| Royal London Short Duration Credit | -2.50% |

| Sanlam Credit | -2.97% |

| Sector: IA Sterling Strategic Bond | -4.31% |

| Sector: IA Sterling Corporate Bond | -5.77% |

| Artemis Corporate Bond | -5.82% |

| Sector: IA UK Gilts | -7.34% |

| Sanlam Hybrid Capital | -7.55% |

Source: FE Analytics 31/03/22

We have positioned a large proportion of your capital at the short end of the curve; Artemis Target Return, Artemis Short-Dated Global High Yield (ASDGHY), RL Short Duration Credit and Sanlam Credit. All these funds have performed as we would have expected considering the upward moves in yields and have not drawn down far below the 3% mark this year. We believe this is a good result especially due to the relatively high yields you will now receive from these funds on an ongoing basis. Furthermore, we expect the capital value of these funds to recover faster than most as managers will be able to put capital to work at these higher rates as their bonds mature. This is versus a manager who invests in longer duration bonds (also would have been hit harder by increased yields) having to wait longer to invest incremental monies at these higher rates.

Sanlam Hybrid:

Sanlam’s Hybrid Capital fund is worth exploring in more detail due to the relatively high drawdown as seen in the table above. With the fund being more aggressively positioned than most fixed income funds, this is expected in these sort of market conditions. For those interested in the detail I have outlined some of the areas contributing to performance this year below, for those not interested I have summarised.

- Preference Shares make up about 20 – 25% of the portfolio. These are “true perpetuals” having have no identifiable redemption date or call date. Rabobank and Aviva are the biggest positions with yields in this area of the market now between 6.5% and 7.5%. Duration is high at “15 – 20 years” (a contributor to the year-to-date drawdown as yields have risen) but as a long-term high yield hold you are compensated.

- AT1 / RT1 securities make up a further 20 – 25% of the portfolio including names such as Investec, Direct Line, Just and Utmost which now yield between 6% and 8%. Interesting observation from the manager is that where bonds are callable, with a reset rate of 5-year Gilt rates (for example) and bonds are currently trading at a meaningful discount to par e.g. 90 cash price. In this scenario, you either own a long-term floating rate issue which will capture higher bond yields, or the bonds get called at 100 in say 6 to 10 years in which case total returns are increased over less time. Although the drawdown to date is clearly not ideal, the forward-looking return profile is certainly more compelling.

- Legacy Securities make up the remaining 40% of the portfolio with a mix of floating rate and fixed rate assets. This group has been the most disappointing of 2022 in that more redemptions were expected by now although when the manager has been in contact with these banks it is far from clear that their attempts to keep bonds outstanding have been approved by regulators. It is much more that they are waiting to be told to redeem early which will happen when they can issue replacement capital at a sensible price like Lloyds did. This book is now fully discounting bonds remaining outstanding, a scenario which the manager believes is highly remote; a number of positions where the market has written off the chance of early redemption but where we see a much better than 50% chance and where we see relatively high annualised returns available in 2022–24. This is element of the portfolio is particularly nuanced so please let us know if more information is needed.

To summarise, although the fund has drawn down more than most there has been no credit events where capital has been lost. We have kept in close contact with the manager for updates whilst also receiving holdings monthly to review turnover and ensure consistency of narrative. Although we would have preferred a lower drawdown year to date (as would the manager I am sure) the forward-looking return profile looks compelling. A conservative estimate (yield to worst) for the Hybrid Capital fund is 4.9%.

Unicorn UK Income:

In other news we had some good news from one of our managers, Unicorn Asset Management, with the announcement that Royal Bank of Canada was looking to initiate a takeover of Brewin Dolphin with a bid at 60% premium to the previous closing price. At a c.4% position as per last factsheet, this position alone should add 2.4% alone to the Daily NAV.

As the manager has been telling us since Brexit (as well as other UK domestic focused managers) they believe the fund holds high quality assets on multiples that are just too low compared to global peers and the market therefore believing more M&A from overseas buyers is likely to be seen if the market remains at these levels. We will write more on this topic in the coming weeks.

- The content of this document is for information purposes only and should not be construed as financial advice

- Please be aware that the value of investments, and the income you may receive from them, cannot be guaranteed and may fall as well as rise

- We always recommend that you seek professional regulated financial advice before investing