We have a month-long rally underway, the first really sustained rise this year. As always lots of speculation as to whether it will last and plenty to worry about, this is very normal! As we pass the halfway mark of 2022 it is worth considering the relatively big adjustments in all markets, caused primarily by inflation. Inflation is back and on everyone’s agenda after decades of relatively low levels. With this in mind, we’ll analyse the outcome of defined benefit pension transfers over time.

It was expected to come and go very quickly after Covid and there are signs in commodity markets that goods inflation is peaking as supply bottlenecks start to ease. This is probably one of the contributing factors to this recent rally in equity markets. On the other hand, however, the US economy in particular, is running ‘hotter’ than expected with a very strong labour market and inflation once embedded is quite hard to stop as witnessed by the wage bargaining going on in the UK right now.

Risk-free rates on longer dated Government bonds are up, with the capital value of UK gilts down by 14% this year as a result, the biggest drop I can remember and a great reminder of why we have called them the ‘return free risk’ rather than the ‘risk free return’ over the years. They still only yield 2.6% and are still a no-go zone for us at current levels.

Our high yield bond funds are also down similar amounts but are now yielding 6% and more, so the interest we earn should recover our losses much quicker.

The more speculative end of equity markets has fallen heavily this year the US Nasdaq is off 25%, whilst value stocks and shares in companies who can pass through inflation or have inflation linked contracts, such as infrastructure companies, have fared much better. We had an excellent investment committee yesterday with TS Lombard’s Martin Shenfield and will report in more detail on our outlook for all these areas in the next update along with any changes in portfolios we decide to make.

Defined Benefit Pension Transfer Update:

For this update I wanted to look specifically at income generation and the impact of these changes as well as recent investment returns for those who completed Defined Benefit (DB) pension transfers with us.

We know this is not everyone, but it is a large majority and the issues here read across to anyone fashioning their retirement income from an invested lump sum which pretty much covers all our clients. It is around keeping up with inflation and our ability to use that lump sum to generate long term income.

Starting with inflation: Whilst there are two measures of inflation RPI and CPI, most DB schemes are linked to CPI not RPI and with RPI due for the chop in 2031 it seems most logical to focus on CPI. As can be seen below UK CPI was running at around the Bank of England’s target rate of 2% from 2016 through 2020. Then we get the post Covid effect.

UK CPI:

For the full year 2022, the CPI figure is going to be much higher, with this number standing at 9.4% for the 12 months to June. As inflation is now outstripping most DB scheme benefit increases, usually capped at 5% in any year (sometimes lower), most DB pension holders are going to see a real and likely permanent loss in the purchasing power of their pensions this year.

If we assume an increase of 2.5% for the first half of 2022 and compound the annualised CPI numbers from 2016 through 2021, most DB pension holders (deferred or in payment), will see an increase of approximately 18% from the summer of 2016 to now.

Then we look at Gilt yields:

20 Year Gilt Yields:

Gilts have jumped from a low of around 0.5% to touch 3% in 2022, they have fallen back a bit but still sit at around 2.7%. This yield increase feeds into corporate bond yield increases, with most bond yields now up 20% from mid-2021.

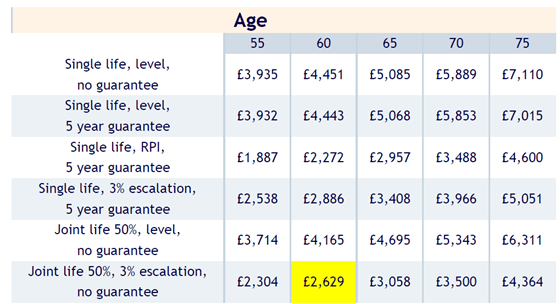

This then feeds into annuity rates: Annuity costs have fallen sharply in 2022 the cost of buying a 3% escalating annuity which is a decent proxy for a limited price indexed DB pension has fallen 22% since the Summer of 2016 as shown in the tables below from the Hargreaves Lansdown annuity web pages and the same chart clipped from one of our transfer reports in July 2016.

Annuity Rates Summer 2016

Annuity Rates Summer 2022

The gain in income buying power is 22% obtained by dividing today’s rate by the 2016 rate (£3,179/£2,629).

Then we look at what our pension holders have earned net of all fees from their investments. The good news is that all three of our flagship portfolios and despite recent corrections have made decent amounts of money.

Between 15% and 29% for the six years net of all fees. Not as much as we would like (it never is) but not too bad after a big correction as we have just endured. Satisfyingly these are above the benchmark returns for the same periods. We look at the IA Cautious Managed 0-35% sector and IA Balanced 40-60% sector, where the percentages relate to equity content in line with our three portfolios. These are up 8% and 18% respectively.

Tideway investors have done better than these benchmark returns after all fees. Or put another way your advice and service from Tideway and the costs of your pension account, dealing and custody have been more than covered by above average returns.

By looking at these returns versus typical increases in DB scheme benefits and multiplying them with the increase in annuity rates we get a sense of how your pension pots risk free income purchasing power has increased in six years relative to the pension left behind in the transfer.

The gain in income buying power is 22% obtained by dividing today’s tare by the 2016 rate (£3,179/£2,629).

Then we look at what our pension holders have earned net of all fees from their investments. The good news is that all three of our flagship portfolios and despite recent corrections have made decent amounts of money.

Between 15% and 29% for the six years net of all fees. Not as much as we would like (it never is) but not too bad after a big correction as we have just endured. Satisfyingly these are above the benchmark returns for the same periods. We look at the IA Cautious Managed 0-35% sector and IA Balanced 40-60% sector, where the percentages relate to equity content in line with our three portfolios. These are up 8% and 18% respectively.

Tideway investors have done better than these benchmark returns after all fees. Or put another way your advice and service from Tideway and the costs of your pension account, dealing and custody have been more than covered by above average returns.

By looking at these returns versus typical increases in DB scheme benefits and multiplying them with the increase in annuity rates we get a sense of how your pension pots risk free income purchasing power has increased in six years relative to the pension left behind in the transfer.

| Tideway’s mixed Asset Portfolio | Total Return Summer 2016 to Summer 2022 net of all fees | Gain relative to scheme benefit increases | Gain in risk free income purchasing power versus scheme benefits |

| Moderate | 29% | +13% | 38% |

| Balanced | 19% | +3% | 25% |

| Cautious | 15% | -1% | 21% |

The transfers you received were at a discount to the risk-free costs in 2016 of buying those benefits, that’s how transfers are calculated.

However, whilst I am not recommending you all go out and buy annuities (I’d be out of a job!) this gain will mean that many of you already have the best of both worlds. You can stay invested and take advantage of the flexibility and potential for further real investment gains in years to come.

Of course, these gains are more prominent now than at the start of 2022, with both bond and equity markets falling. Or, and assuming you haven’t spent too much, you can buy risk free lifetime income with an annuity which will give you a bigger pension than you surrendered in the transfer.

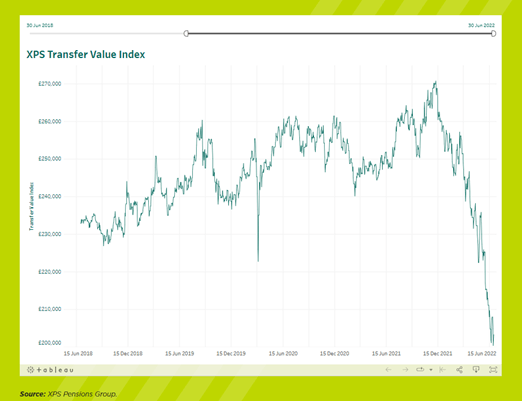

Finally, we can look at the current cash equivalent transfer values of those who have retained their DB pension benefits but may be now considering their options.

According to XPS Pension Group’s Transfer Value Index, the average at month’s end was £203,000, the lowest level since November 2014, as long-term gilt yields continued to rise. They are down 22% from summer 2016 levels Index approximately £260,000. Inline with the drop in annuity prices as you would expect.

So, whilst benefits are up 16% multiplying by the drop in value to income would see most transferees offered around 6% less today than in 2016. Tideway transferees of the Summer of 2016 are 21% to 383% ahead depending on the portfolio used.

For those of you who recall the detailed advice process you went through, you will know Tideway forecast both real investment returns after fees, and an increase in gilt years as we recovered from the great financial crisis of 2008/9. We got the former pretty much immediately but have had to endure quite a bit of volatility along the way. We can expect that to continue but remain confident in the long term returns we can expect.

The gilt yield rise took a while longer to a materialise in fact it went down not up to start, with 2020 and the impact of Covid creating the lowest rate and what looks like the top of the bond market rally which had endured since the 90’s. However, come it did and most market watchers including our colleagues at TS Lombard still expect if to go up a bit more before we can say things are back to normal.

To find out more about cash transfer values, you can use our simple CETV calculator which will provide an estimate of the range of transfer values you might get offered based on your DB pension value.

- The content of this document is for information purposes only and should not be construed as financial advice

- Please be aware that the value of investments, and the income you may receive from them, cannot be guaranteed and may fall as well as rise

- We always recommend that you seek professional regulated financial advice before investing