Barring any significant developments in the next few days this will be our last update for 2021. A good time to take stock of recent events and start to look forward to 2022.

Looking back investment returns this year have been strong and more than we expected coming into 2021. Returns have been driven by US equities, commodity price increases, which have fed into some of the more traditional value equity stocks, global real estate and pockets of Asia and Emerging Markets, with Indian equities topping the return charts.

Returns have been held back by Chinese equities, an increasingly valuable market and influence on global equity returns, which fell 5% over the year, and bonds. As Tideway investors know there are bonds and there are bonds. Generally corporate bonds made no money in 2021, Government bonds lost around 3%, Tideway’s higher yield bonds have made around 3-4% and index linked bonds did very well.

The undeniable efficiency of vaccines along with relatively loose monetary policy and the heavily reduced values of many less growth-orientated companies as we entered 2021 have lifted the value of most companies through the year. Political intervention in China and the continued impact of travel restrictions have probably been the biggest anchors. Shares in Alibaba, one of China’s biggest ecommerce companies, and AIG, parent to British Airways, are both substantially lower in 2021. By contrast Microsoft has climbed around 50% and US oil giant Chevron around 30%.

Tideway Portfolio Returns

Tideway’s Balanced multi asset portfolio (DD3 in shorthand) is up around 10% in 2021 to date after all fees. Added to the 2019 and 2020 returns this portfolio is up just over 30% in three years. The most successful thing we have done is stay invested. That three-year return masks some huge volatility along the way and the subsequent rebound has been accompanied by many ‘nay sayers’: “US equities are too expensive”, “traditional businesses are over”, “the day of reckoning is coming…buy gold”. The biggest mistake investors can make is to try and outsmart markets by way of market timing. Whether that’s trying to time investment moves around the sort of 30% drop in almost all investments we endured in March 2020, or holding back from investing on the view that markets are too high. There is always someone crowing after the event that they got it right, but they rarely refer to all the times previously they got it wrong!

We are more committed than ever to our long-term approach:

- stay invested

- do our due diligence and invest in the best managers we can find, who in turn try and invest in the best assets

- diversify

- plan how to meet your cash withdrawal needs – don’t be a forced seller

We should remember these points when portfolios next drop as they surely will. Your money is invested because you can’t spend it all at once and we want it protected against inflation over the long term. Volatility is just part of that process we should embrace it and plan around it, not be fearful of it.

With the benefit of hindsight, we could have held even more US equities and had less Asia and Emerging equity market exposure, but looking forwards this spread feels right. Avoiding low risk bonds has been very good and our alternative fund holdings in property, infrastructure and multi assets have generally beaten our bond funds, endorsing this allocation.

We are continuing to monitor and manage the more pessimistic outlook for bonds which we will be continuing to focus on in 2022.

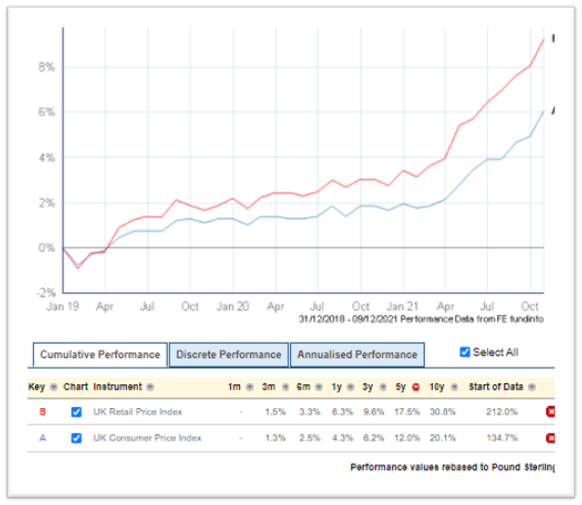

Which brings me to my chart of the year:

UK Inflation since 01.01.2019

Before every update I usually start in FE Trustnet, a chart can say a thousand words! Above, my pick for today’s update – UK inflation.

There has been roughly double the level of price inflation in the UK in the last 10 months than in the previous two years and it equates for roughly half of all the rise in prices of the last five years. The good news is that our three year portfolio returns have been well ahead of these increases.

If inflation runs at 4-6%,and if it is sustained, and that’s probably still quite a big if, it will be something we have not experienced since the turn of the Century. Those of us old enough to have grown up in the 70’s, 80’s and 90’s will remember what ultra-high inflation does. Debts get shrunk in real terms, cash deposits fall in real value and the FTSE 100, launched at the value of 1,000 in 1984 rose to 7,000 by the end of 1999, 700% capital growth in 16 years.

Broadly speaking, higher inflation, if sustained, will be good for equities in the long term, although may make them more volatile in the short term as interest rates rise. It will be good for real assets like property whose prices generally keep in step with inflation. It will be a head wind for bonds until interest rate rises are over.

In the US the FED has largely dropped references to temporary inflationary effects and is talking more about sustained inflation, a change in tone our economic analysts TS Lombard have picked up on.

This will be a key area for us to focus on next year both in our portfolio management but also in engaging with you to make sure you have the right portfolios in the right accounts. Think about what money you will need in the short term, longer term and as a regular income and discuss this with your wealth manager. With higher inflation our lower risk bond portfolios become higher risk for the long term and by contrast our higher risk portfolios with more equities and real assets become lower risk in the long term. Cash deposits are an absolute no no, except for the very short term and for emergencies.

Defined Benefit Pensions

I deliberately put in the two measures of inflation RPI and CPI in the chart above, noting that RPI will be phased out in 8 years’ time and all inflation linkage will be to CPI. CPI has historically run lower than RPI which includes housing costs not included in CPI. This of course is well known to consulting actuaries and employers who sponsor Defined Benefit pension schemes. Many such employers have already moved pension increases in deferment and payment from RPI to CPI to save money as well as dropping the caps on increases from the traditional 5% to 3% and in some cases to 2.5% per year. Those with defined benefits capped at 2.5% have endured a 3.8% drop in their real pension income in the last 12 months, a drop which will likely be a permanent and unrecoverable. Ten years of that would permanently knock 29% off your pension income in real terms.

If you are reading this the chances are that this is no longer a worry for you!

On that happy note, it just leaves me to wish you a festive end to the year. Please do email me at james@tidewayinvestment.co.uk if you have hated the updates, loved them, have topics you would like me to write on, or you have thoughts on how Tideway could improve. We do have some more investment manager interviews lined up for 2022 which we know were popular. It would great to read your feedback in the next few weeks and I hope to see as many of you as possible face to face in 2022!