For those of you who read the financial press there has recently been a number of articles on the demise of the 60/40 traditional managed portfolio, 60% in equities and 40% in bonds.

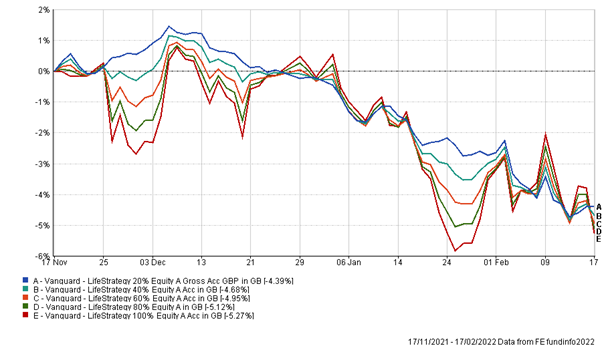

The last couple of months show us why. Here below Vanguards range of ‘Lifestyle’ funds that supposedly allow investors to select the level of risk they want.

As the chart beautifully illustrates, right now it does not matter which portfolio you chose, all portfolios are broadly down the same during the past 3 months.

Figure 1: Vanguard Life Strategy Funds

You could look at the longer-term numbers and say why bother with bonds at all? They have clearly diluted 10 year returns almost by half if you invested 50/50 and short-term, they are offering no protection whatsoever.

It’s a strong argument.

So Why Continue to Hold Bonds?

One of the main reasons we continue to hold bonds is to increase the likelihood of returns over a 2-5 year period. It means the period it will take from any sell-off in asset prices, to get back to a positive return is generally quicker in portfolios with bond exposure than those without. Plus, we try and do this without diluting longer term returns by focusing on the higher yield end of the market.

It’s not to try and limit short-term volatility in the portfolio, as low risk bonds have historically been able to do, that’s not likely to work anymore and it certainly hasn’t worked in the last 3 months.

This strategy is central to Tideway’s mixed asset portfolios designed for those drawing income or about to draw income from the portfolio. The core bond funds we use to do this are the two Sanlam funds and the chart below clearly shows how differentiated they are from they are from either gilts or lower risk corporate bonds. I can’t resist a little dig at Vanguard, there is over £8bn in those two funds which shows the power of marketing and the draw of lower fees over sensible intelligent investing.

Figure 2: Sanlam Hybrid and Credit Funds vs Vanguard Gilt and UK Bond Funds

Sanlam’s Credit fund is doing a good job at holding value thanks to a very short duration approach to the bonds it holds. The higher return targeting Hybrid Capital fund, having held on quite well, finally succumbed to some volatility last week. I spoke to the manager of this fund this week and he advised patience. He has been able to reinvest some maturing bonds at yields over 6% p.a., rates which have not been available for the last few years. These higher interest payments will feed into higher quarterly income distributions and ensure a return to an upward total return curve as soon as capital values stabilise.

It is these interest payments from solid financial institutions, institutions which will benefit if interest rates rise, that will underpin returns. The Sanlam Hybrid Capital fund has returned 5.5% p.a. compound from its launch and if rates start to increase now, we should ultimately see this annual return rate tick up.

I stress again that these bond fund allocations are about stabilising returns over a 2-5 year period. We have, of late, grown accustomed to equity markets rising, even the 2020 Covid induced crash was over within months. However, this hasn’t always been the case.

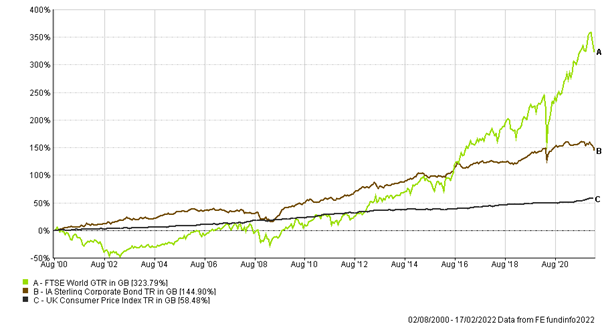

Those unfortunate to invest in global equities just after the Millennium had to wait over a decade to get a decent positive return, 13 years to get ahead of inflation returns and 16 years to catch up with bond investors. Sometimes it pays to be a tortoise, not the hare.

Figure 3: FTSE World Index versus UK CPI, and IA Sterling Corporate Bond

Our two core bond funds are doing much better than the average corporate bond fund, so that tips the balance even further towards these strategies versus higher risk equity strategies.

It is still not clear to us how the next few years play out. Will inflation stay at current elevated levels, rise further or fall back again? Will interest rates normalise to offer real returns again as they did at the Millennium? They have an awful long way to rise! Or, will we get recessions induced by higher energy costs and the first rate rises in almost 20 years resulting on the easy money tap being switched on again. We don’t know and others can only speculate.

It’s worth noting the last base rate rise cycle in the US occurred between June 2004 and June 2006 when base rates rose from 1% to peak at 5.25%. Looking at the chart above, bond funds did quite well to hold and increase value in this period, a c5%-6% p.a. annual return from here from the Sanlam Hybrid Capital fund might turn out to be very attractive compared to equities over the next 2-5 years.