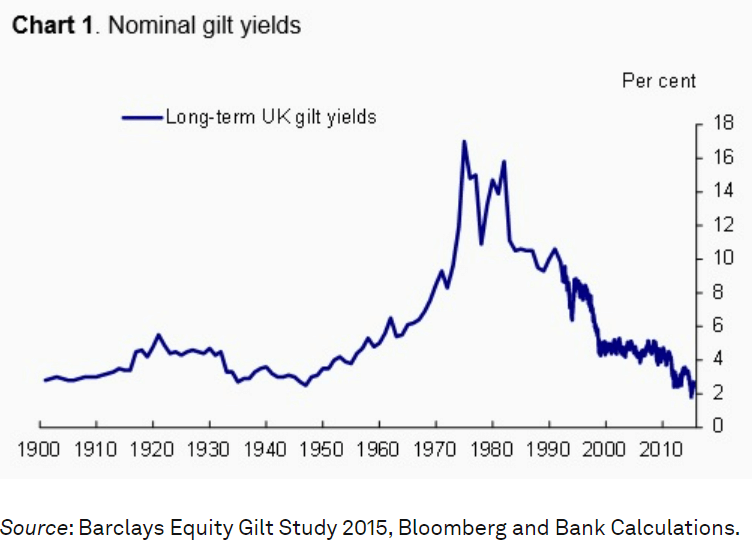

It is often more obvious as the mist clears and when you are looking in the rear-view mirror as to what has been, and is going on.

The summer of 2020 may well mark the bottom in UK gilt yields and the end of a bull market in treasury bonds which had been on the rise since the mid 70’s having previously been on decline since the second World War.

Looking more closely over recent years, first the 2008/9 financial crisis, then Brexit in 2016 and Covid in 2020 kept the downward pressure on as central bankers pumped money to keep economies going. It worked.

The end of Trump, the announcement of the vaccines in the Autumn of 2020 and the subsequent strong recoveries in demand coupled with supply shortages driving inflation, have clearly marked a rise in gilt yields.

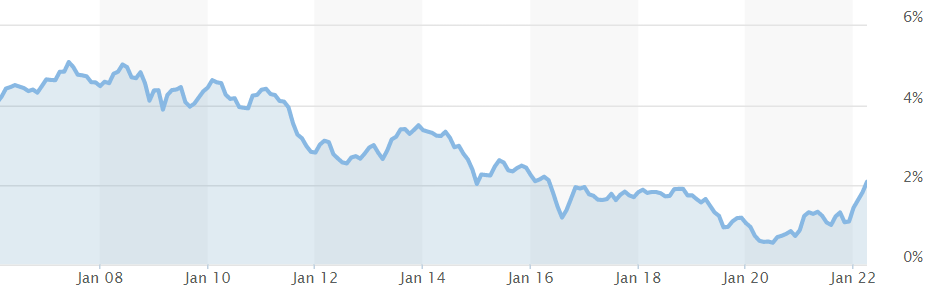

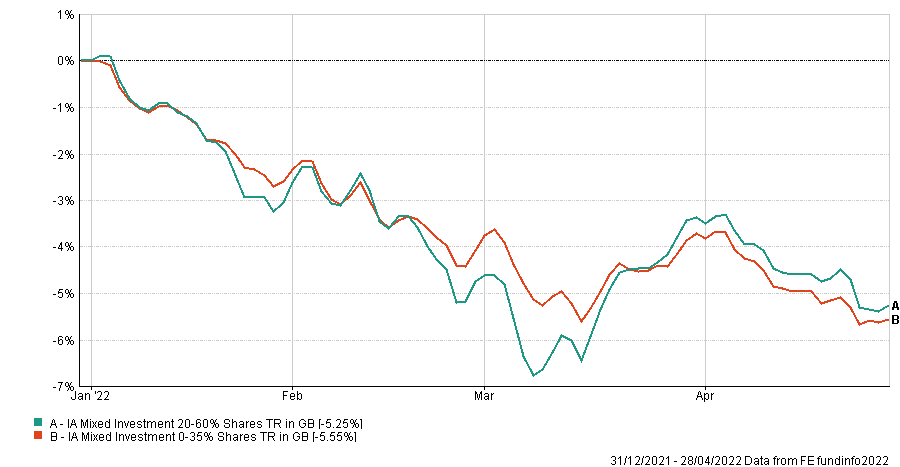

According to Trustnet UK gilt funds, typically seen as defensive safe holdings, are down 8% year to date. Index linked gilt funds, which are harder to understand, are down 11%. We have been wary of investing in UK gilts for a decade, for 8 years we were wrong, now we are right! The decline in gilts is inverting traditional investment risk ratings and I noted whilst reading the data on Trustnet today, the more cautious 0-30% mixed asset fund sector has lost more than the higher risk balance 20-60% equity sector in 2022 so far. Strange times.

Source: FE Analytics 29/04/2022 – Note: Performance figures shown are based on Bid-Bid returns.

| Calendar Performance (%) | |

| Instrument | YTD |

| A IA UK Gilts TR in GB | -8.76 |

| B IA UK Index Linked Gilts TR in GB | -11.31 |

| C UK Consumer Price Index TR in GB | 1.74 |

Source: FE Analytics 29/04/2022 – Note: Performance figures shown are based on Bid-Bid returns.

We should say this rise in yields has only been over the last 18 months or so. We won’t be able to really confirm the bottom until yields normalise. Most commonly they sit just above inflation so if they get to around 3% and inflation falls back to below 3%, we could have more normal market conditions.

Declining treasury yields are typically a strong driver of equity markets, so too is inflation, as equity market returns typically exceed inflation by 4-5% per year on a long-term average basis. But in the short term these adjustments can be painful, that is what we are going through right now. The MSCI world index is also down 11% this year.

Extremely low interest rates, coupled with enormous momentum in certain areas of the market during the Covid lockdowns undoubtedly caused a bubble in some areas of the market and significant under valuations others, both of which are increasingly visible.

This quarter’s earnings releases are highlighting the speed with which markets correct valuations once momentum vanishes and the reality of the need to create increasing profits to support valuations comes into focus.

A few examples:

Netflix

I’m sure that Netflix is a great company. It has a huge global and loyal user base and has created some very fine entertainment in the last decade. By the Autumn of 2021 swept up in the lock down mania and without people much caring about earnings, it got to a £300bn market cap and was trading on an 80X price to earnings (PE) ratio. Today with analysts much more focused on current profits rather than prospect earnings and after last week’s earnings call in which it highlighted falling user numbers, its shares are down 70% since their peak. It is worth just $90bn and is trading at a much more sensible 17x PE ratio.

Microsoft

Not all growth stocks have been hit so hard. Microsoft, which we also think is a great company is down 19% from its peak value. It has risen 6% since its earnings call this week in which it announced estimate beating profits and an 18% year on year revenue growth. At just over $2trillion value it is trading on a 30 x PE.

BP

You can have views on the merits of oil businesses in the long run, but BP is also a great energy company. In Autumn 2020 after the bottom in oil prices that year, the mighty BP was being valued at $35bn, roughly a third of its value two years earlier in 2018. As normality returns and with a recovery in oil prices, BP has doubled in value and is up around 10% in 2022 so far. It just announced record profits of almost $13bn in 2021 and still only trades on a 13x PE.

Three companies making good profits, one hugely expensive (NFLX) has become much more sensibly priced. One expensive (MSFT), continues to be expensive but has revenue and profit growth to justify the price. One dirt cheap (BP) just got more sensibly priced and doubled investors’ money in the process.

The message here is that successful investing is not just about finding good companies but finding them at sensible valuations relative to their current profits and profit growth potential.

Potential Portfolio Moves

For those regular readers of these updates the above analysis is not a new revelation to the Tideway investment team. We are trying to steer a course to avoid bubbles but be diversified across both growth businesses and dividend generators.

We met this week as the chance of a short-term fix for Russia and Ukraine unfortunately diminishes and the inflation/yield increases story continues. We think both will be with us for a while.

We are considering moves and the right opportunity to increase our exposure to the US economy due to its distance from the crisis in Europe and to reward managers who are getting the value considerations just discussed right.