The recovery underway at the end of May reversed sharply last Friday. The US Nasdaq index, at the heart of falling indices in the US and Globally has fallen 12% in the last 5 trading days, although a bounce looks set for today’s session. As of yesterday’s close, it was down 34% from its peak in November 2021 with the broader S&P 500 index officially in a bear market down 24%.

Getting Things in Context

Here are a few things to look at to put things into context:

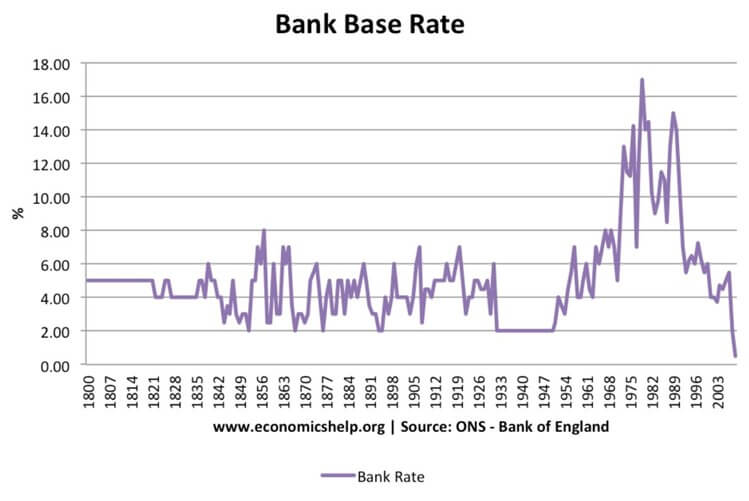

- Base interest rates have been moved up to 1.25% in the UK and 1.5% in the US, it’s still 0% in Europe. By any standard these are still very low rates. As you can see below, taking out the very high rates of the 70’s and 80’s and low rates post the financial crisis, rates have typically been between 2% and 6% with an average rate of 4%. So, these rises are heading towards more normal rates, they are not extreme by any means, just higher than most investors are used to.

Market Analysis:

- UK Gilt and US Treasury yields have risen sharply in recent weeks – the UK to 2.7% and the US to 3.5%. The average yield on 20-year US treasuries has been 4.4% according to YCharts, this rate is getting closer to normal.

- According to Yahoo Finance, the US Nasdaq down 34% has only handed back two years of returns and is still up around 67% over five years.

- Not everything is falling like the Nasdaq. There were few things up in the last week, but year to date the FTSE 100 index of UK shares and the average global equity income fund are only down around 6%.

- Investors in our flagship Balanced Multi Asset Fund are still up around 27% since its inception in September 2016, approximately 4.5% p.a. net of all fees. In a period when there was no return from deposit accounts.

The pain of losing money does not get any easier, even with considerable age. Talking to colleagues and clients in the last few days, who have all been through this before many times, it is still a very painful experience. But the pain will pass.

We believe the return from here for investing in global equities for the next five years will now be significantly higher today than it was from the start of the year.

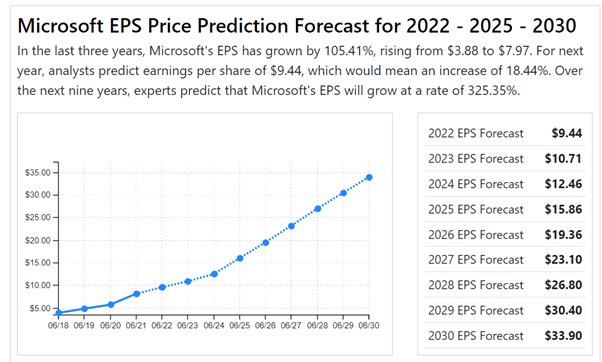

To make my point, let’s look at one of our bell-weather companies, Microsoft. According to the website Stock Forecast and updated as of today, analysts’ consensus view for the company’s forecast earnings per share is shown below.

Microsoft value is now c25 X earnings, on the same basis the shares in 2027 would value at $560. Hitting that price from today’s $247 a share would give a return of 126%. From the November 2021 peak price or $349 the return would be 60%.

Please note analysts’ estimates are just that, estimates that carry significant risks. They should in no way be construed as certain outcomes. This said we are confident we will see those end of year portfolios values again and higher, its only a question of patience.

Our higher income yield and segregated asset approach really comes into its own in conditions like this. Income yields have not diminished, if anything they are rising as our bond managers get to invest new cash and maturing bond proceeds at higher rates.

We will not be forced sellers of any funds currently marked down, we can wait for them to recover meeting withdrawal needs from income, and the shorter dated bond funds where required. We have planned for and are set up to manage through until the pain passes.

Portfolio Changes: Nick Gait

We have made minor tweaks this week in all multi asset portfolios, reducing weightings in Sanlam’s Hybrid Capital, Credit and Multi-strategy funds.

Despite the trimming of these names, we maintain conviction in the managers with these moves motivated primarily by risk management and the continuation of the diversifying our fixed income holdings, which we have been doing gradually over the last couple of years.

Given the current macroeconomic environment we think this is prudent with the added diversification helping to protect on the downside should markets continue to tumble with the broader sector exposure being particularly beneficial.

The replacement funds should be familiar to most of you with these funds already held in Tideway portfolios; Royal London Sterling Extra Yield, Artemis Target Return Bond and Ruffer Diversified Return fund.

It is important to note that although we are selling the Sanlam funds after a period of negative performance, the strategies we are reinvesting your monies in have also declined in value this year and are similar in terms of asset class with risks which are not materially different. Top-down asset allocation remains the same.

Royal London Sterling Extra Yield: Broader sector exposure

The fund has protected capital exceptionally well year to date falling in value by just 3.88% with the fund benefitting from its broader sector exposure than Sanlam’s Hybrid Capital fund.

The fund owns the debt of a diversified range of companies including offshore services businesses and energy businesses which have all benefitted from the rise in energy prices.

Debt of infrastructure groups and miners have also been strong performers year to date in an overall market which has struggled to deliver returns as yields rise and spreads widen.

Like the Hybrid Capital fund, the fund has lower sensitivity to government bond yields and higher sensitivity to sentiment in corporate bond markets. As the name of the strategy suggests the fund has a healthy yield with this twelve-month figure currently 5.78% according to Morningstar.

Artemis Target Return: Ability to make money as rates rise

An alternative to traditional long only short-dated bond funds such as Sanlam Credit which is our major holding in the short-dated space. Very different return profile to long only fixed income with the ability to short positions in Credit and Rates ‘modules’ meaning money can be made irrespective of the direction of rates.

The manager has a long track record of protecting capital with this year being no different with the fund falling just 4.29%, an impressive feat considering the how much yields have risen this year.

Ruffer Diversified Return: More downside protection

The primary aim of the fund is to protect capital in all market conditions. Although the absolute return sector has failed to do this over the last 10 years, against a backdrop of strong performance from most asset classes, Ruffer’s strategy has not.

Going back to 1994, the firm has an almost perfect track record of protecting capital with only one year of negative performance (-0.3%, exceptionally impressive when you think they have managed money across the dot.com bubble, Credit crisis and Covid-19 crisis), and unlike most funds in this sector, the fund has produced equity like returns, annualizing 9% per annum since 1994 with volatility much lower than global equity indices.

The repeatability of the investment process, along with the retention of key staff leads us to believe that it is possible that their success will continue. Although we have not held the fund through the whole period, it has returned 2.41% year to date.

To read previous versions of this market update visit our News & Insights.

- The content of this document is for information purposes only and should not be construed as financial advice

- Please be aware that the value of investments, and the income you may receive from them, cannot be guaranteed and may fall as well as rise

- We always recommend that you seek professional regulated financial advice before investing