There are some mixed messages out there on inflation, growth and interest rates, but almost all of our funds have been rising in value over the last few days, even the bond funds, you will be pleased to hear. As is often the case, the bond fund recovery has lagged the recovery in equity markets.

Global growth is slowing, inflation remains high, but commodity price falls suggest the worst might be over. The Bank of England raised rates yesterday, the most significant raise this Century. It will hurt if you have a variable rate mortgage, but the loan will probably still be free money in real terms after inflation.

If you have cash reserves, it is going to make sense to shop around. Do call us for help on this; we keep an eye on deposit rates and will help you get the best rates – no charge, all part of the service.

Predicting what will happen next in the short term is as always nigh on in possible, that’s why we stay invested.

To quote the Bank of England website:

“How high will interest rates go? We will take the actions necessary to bring inflation down to 2%.

Precisely where interest rates will go depends on what happens in the economy and what we think will happen to the rate of inflation over the next few years.

So we can’t say now exactly how high they will go. But they are not likely to reach the very high levels that some people experienced in the past.

We review how the economy is doing and whether a change in interest rates is needed eight times a year (roughly every six weeks).”

I think ‘some people’ is a way of saying people over the age of 50!

Rightly or wrongly Government bond markets are already beginning to price at the top of rate rises as can be seen here, the UK 20-year gilt yield, which started to fall pretty much in line with the recovery of equity markets.

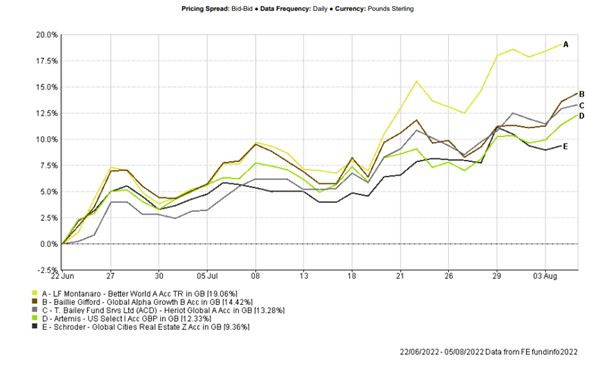

Top Performers:

The recent bottom of equity markets came in around the last week in June and the charts below highlight our best and worst performing funds since this inflection point.

Trying to time equity markets would have been an expensive mistake, in just 6 weeks (a reminder that recoveries can happen very quickly). Of course they could go down again, but over the long term they generally go up. Strong earnings from Microsoft and Alphabet (Google) highlighted that some companies can survive inflation, which will feed into both their top line revenues and bottom line profits in due course. Our global smaller companies fund from Montanaro is up almost 20% in those weeks as I write.

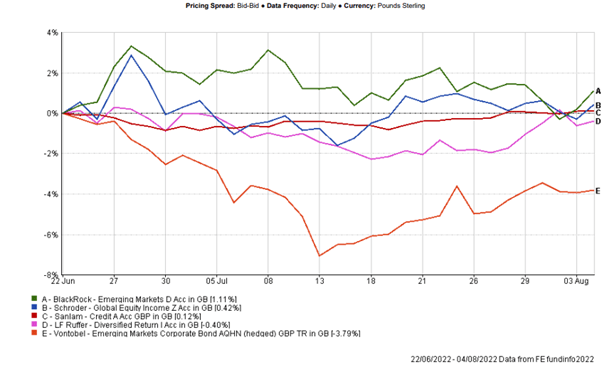

Worst Performers:

‘Losing’ funds since the end of June are showing much smaller losses than the gains hence the rise in portfolio values across the board. As can be seen here, it took until mid-July for some of the bond funds to start to recover.

We are constantly monitoring all the funds we are investing in. Nick Gait has been visiting and interviewing fund managers recently, particularly those who continue to fall to see what is going on.

He has written up some of his findings on Sanlam Multi-strategy for viewing below and will continue to meet managers both current and prospective over the coming weeks and months to ensure we remain fully appraised.

Income yields and total return opportunity from the bond funds, in particular, look very good now on a 3 -5 year basis with yields ranging from 6% per year (Sanlam Hybrid Capital, Royal London Sterling Extra Yield and Artemis Short Dated Global High Yield) up to 9% in the case of the Vontobel EM fund.

Finally, I wanted to highlight Dundas Partners’ Heriot Global fund as one equity fund which has become one of our higher conviction managers with one of our largest weightings in portfolios.

It gets listed under T Bailey on many fund databases, T Bailey is the funds’ administrators, not the fund manager. It is a global equity fund, unrestrained as to where it can invest and seeks out companies that the manager Alan MacFarlane and his team at Dundas Partners in Edinburgh believe can grow their dividends over years to come and ahead of the rate of inflation. It is near the top on recent performance and has delivered great longer-term returns.

From Dundas Global Investors July 19 2022: ‘There is plenty to worry about. We worry most about the corrosive effect of sustained inflation. Dividend growth is the antidote.’

‘Dividend announcements from the Fund’s companies in 2022 to date have been heading in the opposite direction from wilting equity markets.

- Novo Nordisk, world leader in diabetes treatment, increased its dividend per share by 14.2% for 2021 versus the 2020 figure.

- Accenture, the world’s biggest I.T systems consulting and implementation group, raised its dividend per share by 10%

- L’Oreal, the world’s biggest cosmetic group, announced a 20% dividend increase versus its 2021 payment

- Dividend growth is the beating pulse from which we take the health of the Fund’s investments. For 2022 to date 41 of the Fund’s stocks made dividend declarations. 90% announced increased dividends, 10% held at the prior year’s level, and none made cuts. The simple average increase is 18% across all 41 stocks, expressed in local currency, a figure which includes elements of post-Covid restoration and recovery, but the principal driver is underlying business growth.’

I interviewed Alan a few months back and if you have not seen it already I would recommend investing the 45 mins it takes to watch (use the link below), to be inspired about investing in great quality companies and why they offer the best long term protection against inflation.

Click on the link to watch: An Interview with Alan McFarlane, Senior Fund Manager at Dundas Global Investors

I am particularly proud of our investment teams selection of this fund which has outperformed the mighty Fundsmith (the most obvious and most popular choice in this space) over 1, 3 and 5 years according to FE Analytics. Fundsmith has suffered some big redemptions this year and is down around 7% in the last 12 months, Heriot Global is off just 1% over a year.

On top of this Alan is just a really nice guy with decent morals and strong views on responsible investing. We trust him implicitly to look after our money and if he and his team come up short it won’t be through lack of effort.

Sanlam Multi-Strategy – Fund in Focus – Nick Gait

As the name suggests, Sanlam’s Multi-Strategy fund invests in different asset classes to achieve investors’ returns. This approach differs from most of our other managers, who focus on a single asset class or strategy. As such, this is an excellent fund to discuss, providing an overview of the markets of each asset class.

It also has many similarities with how Tideway constructs its multi-asset portfolios and should therefore help understand broader Tideway portfolio returns. The long-term return target of the fund is CPI +4% and aims to achieve this by investing in Equities, Fixed Income securities, as well as Real Assets (the three buckets Tideway uses to construct portfolios). The fund’s mantra is to ‘participate when you can and defend when you need to.’

Under the Sanlam brand, the Multi-Strategy fund is independently run and not beholden to any house view.

The team is headed up by experienced (32 year) fund manager Mike Pingerra. Before joining Sanlam in January 2013, Mike headed up the multi-asset group at Insight Investments and spent 20 years at Credit Suisse in senior positions, including head of special mandates and head of trusts and charities in the asset management and private banking divisions. As head of multi-asset solutions there, Mike managed a team of 14 with responsibility for £5bn of AUM.

Mike is assisted by Fund Managers Johan Badenhorst, who brings dedicated risk management expertise to the team and Christopher Greenland, CFA, who specialises in researching and sourcing real asset investment opportunities. The team also runs a specialist Real Assets fund.

As we have mentioned in previous updates, 2022 has been a challenging period for all investors, with very few conventional asset classes able to protect capital in the current environment of high inflation and slow growth.

The usual government bond equity correlation (typical for the last 20 years) turned positive, meaning risk assets and typically defensive assets such as government bonds have all been trending in the same direction. In addition, the traditionally lower-risk government bonds and fixed income, in general, have been some of the worst performers year to date in the face of rising rates.

2022 has been no different for the Multi-Strategy fund, with all three strategies achieving a negative total return over the period. Real Assets contributed a return of -1.46%, Global Equity -4.20% and Fixed Income -3.60% to portfolio performance to the end of June. The Real Assets and Global Equity primarily performed as expected, whilst the Fixed Income allocation, usually so stable considering the short duration positioning, caused the portfolio to draw down more than expected year to date.

Real Assets:

Focus on long-life operational assets with contractual revenue streams with inflation linkage. These characteristics are supportive of long-term portfolio income and capital growth.

- Infrastructure: Operational bedrock assets with long-term, defensive, and growing cash flows across economic cycles

- Specialist property: A focus on high-quality and mission-critical assets across sectors delivering long-term defensive rental income streams

- Renewable energy investments: A focus on highly contracted and diversified businesses best placed to capture long-term growth opportunities

This part of the portfolio has performed very well in relative terms contributing -1.46% to total portfolio returns. Specialist property was the main negative contributor whilst renewables posted a slight positive and infrastructure was broadly flat. One major reason for this relative solid performance was the inflation protection properties:

- c.46% Inflation-linked & fixed uplift – Well positioned to capture revenue growth.

- c.31% Periodic market reviews – Favourable demand drivers continue to underpin LFL periodic market reviews.

Despite the inflation linkage, these companies have derated and now trade at the most significant discount since inception—an 8% (2017) premium when launched. In short, inflation-linked revenues have increased, but forward-looking returns are still looking promising.

Equity:

Systematic momentum-based approach

Unlike Tideway’s Equity exposure, this fund’s approach uses derivatives to gain exposure (this is one of the primary reasons the fund employs a specialist risk manager) and is both systematic and momentum based. The overall Equity exposure is, therefore, very dynamic. It has ranged from 9% to 28% over the past 12 months.

The fund will cut risk when the equity exposure hits the lower end of the typical range at about 10% when risk will be added back. At this point, the manager is more concerned about a rally than a drawdown: Should the MSCI World (which the fund broadly looks to replicate) fall another 10%, it would only contribute -1% to performance. Conversely, a large rally would mean the fund does not participate should equity exposure not be added back.

Fixed Income:

Preference for short-duration bonds. YTD bond duration ranged from 2.2 to 2.9 years.

Of the three strategies, Fixed Income did not perform its traditional role in the portfolio of stable returns and was the swing factor in overall fund performance.

The short-duration positioning of the fixed income book (like in Tideway’s portfolios) was not sufficient to offset the marked-to-market moves.

The manager was hoping for yields to rise as yield compression had made some traditional fixed income investments uninteresting from an investment perspective. However, it was the speed of the correction which caught people by surprise.

It must be stressed that there were no defaults or rating downgrades in the portfolio, just marked to market moves. No money will be lost should this trend of no defaults continue, and the manager holds these bonds to maturity, which is the core process.

Although painful in the short term, there is no denying that this is a positive over the long term. The capital value of the fixed income book should recover as the bonds mature and prices pull to par. With roughly 23% of the portfolio maturing in the next year (the manager is already locking in these higher nominal returns), and no signs of any Credit stress, the portfolio is well positioned to recover quickly and continue to reinvest at these higher rates providing higher projected future returns. The manager runs a barbell strategy which means bonds mature at regular intervals.

70% of the portfolio is in fixed income and can be currently split out as follows:

- Money Market (c.23%). Duration 0.55 years & YTM 3.6%

- Investment Grade (c.24%). Duration 3.45 years & YTM 4.9%

- High Yield (c.17%). Duration 3.0 years & YTM 7.0%

As mentioned above, although painful in the short term, the benefit of an increase in interest rates (and spreads) is the ability of the fund to reinvest at higher yields.

Eighteen months ago, the yield on the fund was 1.8%; today, this number is over 4% which more than covers the 3% distribution yield, which is paid monthly. The fund yield has never been higher in the ten years since launch.

As with the short-duration fixed income assets in Tideway portfolios, the higher-than-expected drawdowns contributed negatively to overall returns despite being positioned for rising interest rates.

Although it is painful when looking at asset values on the screen, we are not worried in this instance as the main healer to fixed income returns is time (especially in shorter duration strategies) as bonds recover closer to their maturity dates and the managers can use the proceeds to purchase higher-yielding bonds.

We remain highly constructive on the fund and see a clear path to recovery over the short to medium term with the fixed income book. Longer-term returns are covered by Real Assets, which the manager aims to buy and hold (holding many of the current holdings since the strategy’s inception), providing growth and inflation protection. The Global Equity portion is the balancing strategy, going more defensive when markets sell-off and looking to participate on the upswing.

Should there be any other of our current funds that investors would like us to talk through, please let us know. We meet all our managers regularly and are happy to provide some up-to-date information and analysis upon request.

To read more market updates, check out our News & Insights . If you have any further questions do not hesitate to get in touch here.

- The content of this document is for information purposes only and should not be construed as financial advice

- Please be aware that the value of investments, and the income you may receive from them, cannot be guaranteed and may fall as well as rise

- We always recommend that you seek professional regulated financial advice before investing